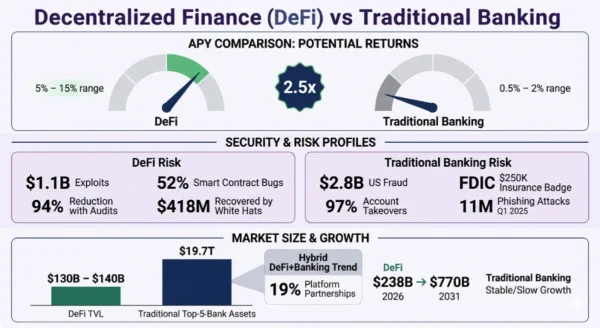

DeFi vs Traditional Banking is the financial comparison defining money in 2026 — not because decentralised finance has replaced banks, but because the line between them is eroding faster than anyone expected. Grayscale Research named 2026 “the dawn of the institutional era” for digital assets: bipartisan US crypto legislation is advancing, the FDIC approved GENIUS Act stablecoin application procedures in December 2025, 71% of institutional investors already hold digital assets, and 19% of DeFi platforms are now formally partnered with traditional banks. At the same time, the contrast between the two systems could not be sharper in the numbers that matter most to users. DeFi settles transactions in 3.6 seconds and offers 5–15% APY on stablecoin lending. The average international bank wire takes 28 hours and charges $25–50.

US savings accounts yield 0.5–2% APY. DeFi protocols have grown from 940,000 users in 2021 to over 20 million in 2025 — a 2,000% increase in four years — while decentralised exchange trading volume hit $462 billion monthly in 2025. The DeFi market stands at $238.54 billion in 2026 and is projected to reach $770.56 billion by 2031 at a 26.43% CAGR. Traditional banking holds $19.7 trillion in assets at the five largest US banks alone. These are not two systems on equal footing — yet. But the DeFi vs Traditional Banking comparison in 2026 is no longer theoretical. It is the infrastructure decision that every fintech developer, investor, corporate treasury, and curious individual needs to understand before committing capital or building products. This comparison covers both systems completely — how they work, what they cost, where each wins, and how to decide which belongs in your financial life.

DeFi vs Traditional Banking: The 2026 Financial Landscape

The DeFi vs Traditional Banking debate has moved decisively from ideological argument to practical financial decision-making in 2026. For years the comparison was framed as disruption — decentralised finance was going to eliminate banks. The reality that has emerged is more nuanced and ultimately more interesting: the two systems are converging at their edges while remaining fundamentally distinct at their cores. DeFi protocols are integrating fiat on-ramps, custodial wallets, and KYC compliance layers for institutional access. Traditional banks are integrating blockchain settlement, stablecoin custody, and tokenised assets into their product stacks. The result is a financial landscape where the question is no longer “DeFi or banks?” but rather “which system for which job, at which risk tolerance?”

DeFi vs Traditional Banking: Traditional Banking Explained

Definition

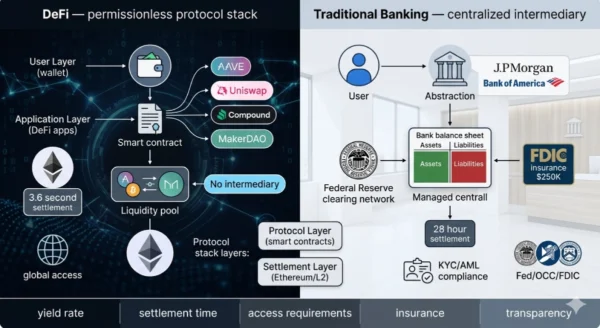

Traditional banking refers to the centralised financial system operated by licensed, regulated institutions — commercial banks, savings banks, credit unions, and investment banks — that accept deposits, extend credit, process payments, and provide financial services under the oversight of government regulators (the Federal Reserve, OCC, FDIC in the US; ECB and national regulators in Europe). Traditional banks act as intermediaries: they hold your funds, underwrite your loans, process your transactions, and guarantee your deposits up to regulatory limits (FDIC insures up to $250,000 per depositor per institution in the US).

In exchange for these safety guarantees and convenience, banks extract value at every layer: the spread between deposit rates (0.5–2% APY) and lending rates (6–30% depending on product), transaction fees, maintenance fees, and foreign exchange margins. The five largest US banks — JPMorgan Chase, Bank of America, Citigroup, Wells Fargo, and Goldman Sachs — collectively hold $19.7 trillion in assets, making traditional banking the largest industry by assets in the global economy. In 2026, the traditional banking system faces its most significant structural challenge since the 2008 financial crisis: the emergence of DeFi protocols offering comparable financial services without intermediaries, faster settlement, and meaningfully higher yields on deposits.

Strengths and Advantages

- Deposit insurance: FDIC guarantees up to $250,000 per depositor per institution in the US — a foundational safety net that no DeFi protocol can match. Bank failures do not result in depositor losses up to this limit

- Regulatory protection: Banking regulations protect consumers from predatory lending, discriminatory practices, and abusive fees — decades of consumer protection law applies to every interaction

- Credit access: Traditional banks can extend unsecured credit based on income and credit history — mortgages, personal loans, credit cards, and business loans without requiring overcollateralisation

- Fiat currency integration: Seamless integration with the broader economy — payroll, tax payments, government benefits, real estate transactions, and everyday spending all run through the traditional banking rails

- Recovery and dispute resolution: Fraudulent transactions can be reversed, customer service escalation paths exist, and courts recognise claims against regulated institutions

- Stability and predictability: Deposit rates, fee structures, and account terms are governed by contracts enforceable in law — service availability (branches, ATMs, customer service) is contractually guaranteed

Limitations and Constraints

- Low yields: Standard savings accounts pay 0.5–2% APY — after inflation, the effective real return is often negative. DeFi stablecoin lending yields 2.5x more than traditional high-yield products

- Slow international settlement: International wire transfers average 28 hours and cost $25–50 per transfer — a structural inefficiency that blockchain settlement eliminates entirely

- Access barriers: 78% of traditional banking institutions in emerging markets still require in-person identity verification — government ID, proof of address, and sometimes credit history exclude the 5.4 billion globally underbanked

- Opacity: Only 34% of banks display service fees and account rules up front — fee structures, currency conversion margins, and early withdrawal penalties are often buried in product disclosures

- Custodial risk: Your bank balance is a liability of the bank, not your property — funds above the FDIC limit are unsecured claims against the institution in the event of failure

- Geographic limitations: 91% of traditional banking infrastructure investment is concentrated in G20 countries — billions of people in emerging markets receive minimal banking service from the global financial system

Traditional Banking Key Parameters (2026):

Assets: $19.7 trillion held by the five largest US banks; global banking assets exceed $180 trillion. Savings APY: 0.5–2% (standard); up to ~4.5% at high-yield online banks. International Wire: 28 hours average; $25–50 fee per transfer. Furthermore, Deposit Insurance: FDIC $250K per depositor per institution (US); FSCS £85K (UK); comparable schemes in EU member states. KYC/AML: Mandatory — government ID, proof of address, in some markets employment verification. Additionally, Regulation: Federal Reserve, OCC, FDIC (US); ECB, EBA (EU); FCA (UK) — comprehensive oversight. Moreover, Settlement: ACH 1–3 business days domestic; SWIFT 1–5 days international; real-time payments emerging (FedNow, SEPA Instant).

DeFi vs Traditional Banking: DeFi Explained

Definition

Decentralised Finance (DeFi) is a system of financial services and products built on public blockchain networks — primarily Ethereum, which commands approximately 68% of all DeFi TVL — using self-executing smart contracts that replace traditional financial intermediaries. Rather than depositing funds into a bank that manages your money on your behalf, DeFi users deposit crypto assets directly into smart contracts that algorithmically manage lending, trading, yield generation, and settlement according to code visible to anyone on the blockchain. The smart contract is simultaneously the bank, the loan officer, the exchange, and the settlement system — all encoded in transparent, permissionless logic that anyone with an internet connection and a cryptocurrency wallet can access, without approval, without credit check, and without geographic restriction.

The foundational DeFi protocols — Aave (lending, $20.38B TVL), Uniswap (decentralised exchange), MakerDAO (stablecoin, 28% lending market share), and Compound (lending, 24% market share) — collectively define the financial primitives that replicate and in some cases improve upon traditional banking services. In the DeFi vs Traditional Banking comparison in 2026, DeFi’s advantages are most visible in yield (5–15% APY on stablecoin lending vs 0.5–2% in banks), speed (3.6-second on-chain settlement vs 28-hour wires), and access (anyone globally vs identity-verified account holders). Its disadvantages are equally visible: no deposit insurance, irreversible transactions, smart contract exploit risk, and a regulatory framework still being actively written.

Strengths and Advantages

- Superior yields: DeFi lending protocols offer 5–15% APY on stablecoin deposits — 2.5x more than traditional high-yield bank products. Swiss-regulated DeFi ETPs target yields of approximately 15% on SOL, 10% on USD, and 7% on CHF within compliant wrappers

- Near-instant settlement: On-chain transactions settle in 3.6 seconds on average — compared to 28 hours for international wire transfers. Layer-2 networks reduce this further and cut gas fees to cents

- Permissionless global access: Anyone with an internet connection and a cryptocurrency wallet can access DeFi — no ID, no address, no credit history required. 86 countries now support on-ramp access to DeFi via local fiat currencies

- Full transparency: 91% of DeFi apps display protocol fees and rules up front — smart contract code is publicly auditable, and on-chain transaction records are permanent and verifiable by anyone

- Self-custody: 89% of DeFi users cite control over funds as their primary preference — assets held in a personal wallet are legally yours, not a liability of any institution

- Composability: DeFi protocols are “money Legos” — they interconnect, enabling complex financial strategies (yield farming, flash loans, automated arbitrage) that no bank can offer and no traditional financial product replicates

Limitations and Constraints

- No deposit insurance: DeFi has no equivalent of FDIC insurance — smart contract failures, protocol exploits, or governance attacks can result in total loss of deposited funds with no recovery mechanism

- Smart contract risk: $1.1 billion in DeFi exploits and protocol hacks in the first half of 2025 alone — 52% of breaches came from smart contract vulnerabilities. Audited protocols experience 94% fewer hacks, but audits are not universal

- Overcollateralisation requirement: DeFi loans require crypto collateral worth more than the loan — typically 130–200% collateral ratio. This makes DeFi borrowing inaccessible for those without existing crypto assets, unlike unsecured bank credit

- Irreversible errors: Transactions sent to wrong addresses, or approved phishing transactions, cannot be reversed — no customer service, no fraud recovery, no regulatory recourse

- Complexity and UX: Managing private keys, understanding gas fees, evaluating audit status, and navigating protocol governance is significantly more complex than opening a bank account

- Regulatory uncertainty: DeFi operates in a regulatory grey zone in most jurisdictions — the legal treatment of DeFi protocol income, governance tokens, and user activity is still being actively defined in 2026

DeFi Key Parameters (2026):

TVL: $130–140 billion in early 2026 (Ethereum: 68% share). Market Size: $238.54 billion in 2026 → $770.56 billion by 2031 (26.43% CAGR). Users: 20 million+ unique users in 2025, up from 940,000 in 2021 (+2,000%). Furthermore, Top Protocols: Aave (lending, ~$20.38B TVL), Uniswap (DEX), MakerDAO (28% lending market share), Compound (24%). Yields: 5–15% APY stablecoin lending; 2.5x multiple vs traditional high-yield products. Additionally, Settlement: 3.6 seconds on-chain average. DEX Volume: $462 billion monthly (2025 record). Moreover, Security: $1.1B exploits H1 2025; audited protocols see 94% fewer hacks; $418M recovered by white hat hackers.

DeFi vs Traditional Banking: Architecture and Technology Deep Dive

How Traditional Banking Processes a Loan

- Borrower submits application with employment history, income documentation, credit report, and collateral details

- Bank’s underwriting team reviews application manually or via credit scoring algorithm — typically 2–7 business days

- Bank lends from its own balance sheet — funded by depositor savings, interbank lending, or bond issuance

- Approval triggers legal documentation, disbursement via ACH or wire, and registration of any collateral (mortgage, lien)

- Ongoing monthly repayments; prepayment penalties may apply; default triggers collection process, credit reporting, and potential legal action

- Bank earns the spread between deposit cost (0.5–2%) and lending rate (6–30%) as net interest income

How DeFi Processes a Loan (Aave)

- Borrower connects cryptocurrency wallet (MetaMask, Coinbase Wallet) to Aave protocol — no identity required

- Borrower deposits collateral (e.g. ETH worth 150% of the loan amount) into Aave’s smart contract

- Smart contract automatically calculates maximum borrowable amount based on collateral ratio and protocol parameters

- Borrower receives requested stablecoins (USDC, DAI) in wallet — settlement in 3.6 seconds, no approval wait

- Interest accrues in real time on-chain; if collateral value drops below liquidation threshold, smart contract automatically liquidates collateral to repay lenders

- Protocol earns fees from the interest rate spread; these fees flow to liquidity providers and Aave’s DAO treasury — no bank intermediary

The DeFi Protocol Stack

| Layer | DeFi Component | Traditional Banking Equivalent |

|---|---|---|

| Settlement Layer | Ethereum mainnet, Solana, or Layer-2 (Arbitrum, Optimism, Base) — final transaction settlement and security | Federal Reserve (FedWire, FedNow), ECB (TARGET2) — central bank settlement infrastructure |

| Asset Layer | Crypto tokens (ETH, BTC), stablecoins (USDC, DAI, USDT) — the money moving through DeFi systems | Fiat currency (USD, EUR, GBP) — government-issued money in bank accounts |

| Protocol Layer | Smart contracts (Aave, Uniswap, MakerDAO, Compound) — the rules encoded in code that govern transactions | Bank policies, loan agreements, deposit terms — rules encoded in legal documents |

| Application Layer | DeFi front-ends and aggregators — Uniswap.org, app.aave.com, DeFi dashboards (Zapper, DeBank) | Bank branches, mobile banking apps, online banking portals |

| User Layer | Self-custodial wallets (MetaMask: 100M+ users, 30M+ MAU) — user’s direct interface to DeFi protocols | Bank accounts — the regulated relationship between customer and institution |

Key DeFi Mechanisms Explained

Automated Market Makers (AMM)

AMMs replace traditional order books with liquidity pools — smart contracts holding two tokens where users trade against the pool algorithmically. Uniswap’s AMM enables permissionless trading of any token pair; liquidity providers earn trading fees. DEX volume hit $462 billion monthly in 2025. No market maker, no broker, no minimum trade size.

Overcollateralised Lending

DeFi loans require collateral worth more than the borrowed amount (typically 130–200%). This replaces credit scoring — creditworthiness is not assessed because the smart contract can automatically liquidate collateral if its value drops. Aave V2 led with $4.1 billion in lending volume; DeFi captured 59.83% of the total crypto lending market in Q2 2025.

Yield Farming and Liquidity Mining

Users earn yield by depositing assets into DeFi protocols as liquidity. Returns come from trading fees, protocol token rewards, and lending interest. The combination can significantly exceed traditional savings rates — hence 5–15% APY on stablecoins vs 0.5–2% at banks. Risks include smart contract exploits and token reward dilution.

DeFi vs Traditional Banking: Use Cases and Real-World Scenarios

Where Traditional Banking Excels

- Mortgage and unsecured credit: Buying a house, financing a car, or getting a personal loan without holding 150%+ of the loan value in crypto collateral — traditional banking’s underwriting model enables credit based on income and history

- Payroll and everyday transactions: Salary payments, direct debits, government benefits, tax payments, and merchant transactions all run through bank account rails — incompatible with DeFi’s on-chain settlement model for everyday use in 2026

- Business banking and trade finance: Letters of credit, trade finance, business lines of credit, payroll management, and corporate treasury operations require the legal enforceability and institutional relationships that traditional banks provide

- Regulated investment products: Pension funds, mutual funds, ISAs, 401(k) accounts — tax-advantaged investment vehicles with legal protections that DeFi protocols cannot replicate in their current form

- Cross-border business payments (established routes): SWIFT and correspondent banking remains the settlement standard for large institutional cross-border transactions where legal recourse and relationship banking matter more than speed

Where DeFi Excels

- Cross-border remittances: Sending money internationally in 3.6 seconds for cents vs a 28-hour, $25–50 wire — the remittance use case is DeFi’s most compelling real-world advantage, particularly for the 5.4 billion globally unbanked or underbanked

- Yield generation on stablecoins: Earning 5–15% APY on USD-pegged stablecoins (USDC, DAI) via Aave, Compound, or Curve — 2.5x more than the best traditional high-yield savings accounts for users comfortable with protocol risk

- Trading and speculation: DEX trading of crypto assets 24/7 with no minimum size, no broker, and no account approval — $462 billion monthly volume confirms this is the primary DeFi use case by dollar volume

- Financial inclusion for the unbanked: 53% of new DeFi wallet creations in 2025 came from mobile-first regions in Southeast Asia and Africa — DeFi is reaching populations that traditional banking infrastructure has never served

- Programmable finance: Flash loans, automated yield strategies, cross-protocol arbitrage, and DAO treasury management — financial operations impossible in traditional banking that DeFi’s composable protocol stack enables natively

DeFi vs Traditional Banking: Profile Match

| User Profile | Traditional Banking Fit | DeFi Fit |

|---|---|---|

| Homeowner / mortgage seeker | High — credit-based lending is exclusively traditional banking | Low — DeFi loans require overcollateralisation, not income-based credit |

| Crypto holder seeking yield | Low — banks offer negligible yield on crypto or none | High — 5–15% APY on stablecoins is the primary DeFi value proposition |

| Unbanked individual in emerging market | Low — access barriers exclude most; 78% require in-person ID verification | High — anyone with a smartphone and internet can access DeFi protocols |

| Corporate treasury manager | High — trade finance, credit facilities, regulatory compliance requirements | Medium — tokenised assets and institutional DeFi pools emerging in 2026 |

| Active crypto trader | Low — no crypto trading support at most traditional banks | High — DEX trading 24/7 with no account minimums or broker fees |

| International remittance sender | Low — 28 hours, $25–50 per transfer, often unavailable to unbanked recipients | High — 3.6 second settlement, cents in fees, accessible on both ends |

| Retiree protecting savings | High — FDIC insurance, stable returns, legal protections, no technical complexity | Low — exploit risk, complexity, and volatility not suitable for capital preservation |

12 Critical Differences: DeFi vs Traditional Banking

The DeFi vs Traditional Banking comparison below covers every key dimension — from custody and access to yields, security, regulation, and the emerging convergence of both systems in 2026.

Aspect | Traditional Banking | DeFi |

|---|---|---|

| Custody Model | Custodial — bank holds your funds as a liability on its balance sheet; your balance is a legal claim on the bank | Self-custodial — your private key, your assets; no institution can freeze, confiscate, or restrict access without your signature |

| Access Requirements | Government-issued ID, proof of address, sometimes credit check and employment verification; 78% require in-person verification in emerging markets | Cryptocurrency wallet and internet connection only; no identity verification for base-layer protocols; KYC available on institutional pools |

| Deposit Safety | FDIC insured up to $250,000 per depositor per institution (US); equivalent schemes in EU and UK | No deposit insurance — smart contract exploits, governance attacks, or oracle failures can result in total fund loss |

| Interest/Yield Rate | 0.5–2% APY (standard savings); up to ~4.5% at high-yield online banks | 5–15% APY on stablecoin lending (Aave, Compound); 2.5x higher than traditional high-yield products on average |

| Settlement Speed | ACH 1–3 business days domestic; international wire 28 hours average; emerging real-time (FedNow, SEPA Instant) | 3.6 seconds average on-chain settlement; Layer-2 networks faster; instant global, no banking hours |

| Transaction Fees | International wire $25–50; currency conversion 2–3% margin; ATM fees; account maintenance fees | Gas fees on Ethereum vary ($0.10–$50+); Layer-2 networks offer cents-level fees; no account fees |

| Lending Model | Credit-based — income, credit score, and collateral determine borrowing capacity; unsecured credit available | Overcollateralised — 130–200% crypto collateral required; no credit check; automatic liquidation if collateral value drops |

| Transparency | Only 34% of banks display fees and terms up front; internal processes, lending decisions, and fee structures are opaque | 91% of DeFi apps display protocol fees up front; all smart contract code is publicly auditable; all transactions are on-chain and verifiable |

| Fraud / Security Risk | $2.8 billion in US banking fraud H1 2025; 11 million phishing attacks Q1 2025; fraud usually recoverable via bank dispute process | $1.1 billion in DeFi exploits H1 2025; 52% from smart contract vulnerabilities; transactions irreversible; $418M recovered by white hats |

| Regulation | Comprehensive — Federal Reserve, FDIC, OCC (US); ECB, EBA (EU); FCA (UK); decades of consumer protection law | Evolving — US bipartisan crypto legislation advancing 2026; EU MiCA in force; FDIC GENIUS Act stablecoin procedures approved Dec 2025 |

| Geographic Reach | 91% of infrastructure investment concentrated in G20 countries; 5.4 billion globally unbanked or underbanked | Available to anyone globally with internet access; 86 countries support fiat on-ramps; 33% of users in Asia, 21% Latin America |

| Convergence Direction | Banks integrating blockchain settlement, stablecoin custody, tokenised assets; PayPal applied for bank charter Dec 2025 | 19% of DeFi platforms partnered with traditional banks; 46% offer custodial wallets; hybrid platforms grew 24% in 2025 |

DeFi vs Traditional Banking: A 3-Phase Getting Started Guide

Phase 1 — Understanding and Setting Up (Both Systems)

Starting with Traditional Banking

- Compare account types — checking (daily spending), savings (yield), money market accounts, and CDs. For maximum yield within traditional banking, high-yield savings accounts at online banks offer the best rates (~4.5% APY in 2026)

- Understand FDIC insurance coverage — $250,000 per depositor per institution; spread deposits across multiple institutions if your balance exceeds this

- Compare fee structures before opening — monthly maintenance fees, minimum balance requirements, wire transfer costs, and foreign transaction fees all affect total cost of banking

- For mortgages and credit: understand your credit score, income-to-debt ratios, and down payment requirements before approaching lenders

- For international transfers: compare SWIFT wire, specialist transfer services (Wise, Revolut), and bank-to-bank options on speed, fee, and exchange rate

Starting with DeFi

- Set up a self-custodial wallet — MetaMask (100M+ total users, 30M+ MAU) is the most widely used. Write your 12-word seed phrase on paper and store it securely offline — losing this means losing all funds permanently

- Acquire crypto via a centralised exchange (Coinbase, Kraken, Binance) — purchase stablecoins (USDC, DAI) for lower-risk DeFi entry without cryptocurrency price exposure

- Bridge stablecoins to a Layer-2 network (Arbitrum, Base, Optimism) to reduce Ethereum gas fees from $10–50 to cents per transaction

- Start with a small amount — deposit $50–100 into Aave or Compound to understand the yield mechanics, transaction flow, and gas costs before committing larger sums

- Check protocol audit status before depositing — only use protocols with recent third-party audits from reputable firms (Certik, Trail of Bits, OpenZeppelin). Audited protocols experience 94% fewer hacks

Phase 2 — Core DeFi Operations

Yield Generation on Aave

- Navigate to app.aave.com and connect your wallet — Aave is the #1 DeFi lending protocol with ~$20.38 billion TVL

- Select “Supply” and choose USDC or DAI — stablecoin deposits earn lending interest paid by borrowers, currently in the 5–10% APY range depending on market demand

- Approve the transaction in MetaMask — pay the gas fee (cents on Layer-2, $5–20 on Ethereum mainnet). Your deposit enters the Aave liquidity pool immediately

- Monitor your aToken balance (aUSDC, aDAI) — these tokens accrue interest in real time and can be redeemed for the underlying asset plus earned yield at any time

- To withdraw, click “Withdraw” — Aave protocols have no lock-up periods; funds are accessible 24/7 unlike traditional bank CDs or notice accounts

Cross-Border Transfer via DeFi

- Sender converts fiat to stablecoins (USDC) at source — via Coinbase, Kraken, or local exchange (86 countries now support fiat on-ramps)

- Transfer USDC directly to recipient’s wallet address — on-chain settlement completes in 3.6 seconds; Layer-2 networks reduce fees to under $0.01

- Recipient converts USDC back to local fiat via local exchange or crypto ATM — available in the Philippines, Nigeria, Vietnam, Brazil and most major markets

- Total cost comparison: DeFi transfer ~$0.01–0.50 vs traditional wire $25–50 + 2–3% currency conversion margin

- For recurring remittances, consider stablecoins held in recipient wallet — they can access DeFi yield on USDC while awaiting fiat conversion, earning interest traditional banking does not provide

Phase 3 — Building a Hybrid Financial Stack

The institutional-era approach (2026): The DeFi vs Traditional Banking choice is not binary for most users. 19% of DeFi platforms now partner with traditional banks. The most effective approach uses each system for what it does best:

- Traditional banking for regulated, protected capital: Use FDIC-insured accounts for emergency funds, near-term savings, and any capital you cannot afford to lose. Keep mortgage and credit relationships with regulated banks for unsecured credit access and legal enforceability

- DeFi for yield on crypto holdings: Crypto assets held long-term in a self-custodial wallet can earn 5–15% APY via Aave, Compound, or Curve rather than sitting idle. This yield on already-held crypto does not require trust in a bank and eliminates the opportunity cost of holding unproductive assets

- Stablecoins for international transfers: Whenever sending money internationally, compare stablecoin transfer cost ($0.01–0.50, 3.6 seconds) against wire transfer ($25–50, 28 hours) — the DeFi option wins on every metric except legal recourse if something goes wrong

- CEX as the bridge: Use a centralised exchange (Coinbase, Kraken) as the fiat-to-crypto bridge — CEXs are regulated, insured, and offer simple onboarding while giving access to the DeFi ecosystem for on-chain operations

- Monitor the regulatory environment: US GENIUS Act stablecoin framework and EU MiCA are defining the legal landscape for DeFi in 2026 — as regulatory clarity increases, institutional DeFi pools with KYC compliance are becoming viable for corporate treasury and larger retail allocations

DeFi vs Traditional Banking: Yields, Fees, Risks and Market Data

Traditional Bank Assets

$19.7T

Assets held by the five largest US banks — the scale that defines global financial infrastructure

DeFi Market 2026

$238.54B

DeFi market size in 2026, projected to reach $770.56B by 2031 at 26.43% CAGR

DeFi Users Growth

+2,000%

DeFi user growth 2021–2025: from 940,000 to 20M+ unique users in four years

Gen Z Preference

57%

Of Millennials and Gen Z prefer DeFi apps over mobile banking for investment transactions in 2025

Yield Comparison: DeFi vs Traditional Banking

| Product | DeFi | Traditional Banking | DeFi Advantage |

|---|---|---|---|

| Stablecoin / USD savings | 5–15% APY (Aave, Compound — varies by demand) | 0.5–2% APY standard; ~4.5% high-yield online | 2.5x–10x depending on DeFi rate and bank tier |

| ETH / BTC yield | 3–8% APY staking (ETH); wrapped BTC in DeFi pools | Not offered at most banks; limited crypto products emerging | DeFi only option for yield on crypto assets |

| International transfer | $0.01–0.50 via stablecoins, 3.6 seconds | $25–50 per wire, 28 hours | DeFi: ~100x cheaper, ~28,000x faster |

| Borrowing rate | Variable 3–12% (overcollateralised only) | 6–30% depending on product (mortgage to credit card) | DeFi competitive for collateralised borrowing; traditional wins for unsecured |

| Trading / exchange fees | 0.05–0.3% DEX fee; gas costs variable | FX margin 2–3%; brokerage commissions; spread | DeFi cheaper for frequent small trades; comparable for large |

Security Comparison: DeFi vs Traditional Banking Risks

| Risk Category | Traditional Banking | DeFi |

|---|---|---|

| Total fraud / exploit losses (H1 2025) | $2.8 billion in US banking fraud — 11 million phishing attacks in Q1 2025 | $1.1 billion in DeFi exploits and hacks — 52% from smart contract vulnerabilities |

| Primary attack vector | Account takeovers (97% of incidents); phishing; social engineering | Smart contract bugs (52%); flash loan exploits (58% of 2025 losses); rug pulls (19% of incidents) |

| Loss recovery | High — FDIC coverage, fraud dispute processes, regulatory intervention, legal recourse | Limited — $418M recovered by white hat hackers and bounty programs; no regulatory backstop for most losses |

| Mitigation | Multi-factor authentication; fraud monitoring; KYC/AML compliance | Protocol audits reduce hacks 94%; circuit breakers; white hat bounties ($112M payouts in 2025); DeFi insurance (Nexus Mutual: $610M in claims) |

| Systemic risk | Bank failures (SVB 2023); contagion risk managed by central banks and FDIC resolution | Protocol failures and liquidation cascades during volatility; no central bank backstop; circuit breakers reduce cascade risk |

The Convergence Reality: 2026 Hybrid Models

Banks are becoming DeFi, and DeFi is becoming banks

The DeFi vs Traditional Banking comparison in 2026 cannot ignore the convergence underway at both ends. Banking API integrations with DeFi portfolios rose 29% in 2025. 19% of DeFi platforms formally partner with traditional banks for fiat on-ramps and off-ramps. 46% of leading DeFi platforms offer custodial wallets — a traditional banking feature. Hybrid DeFi/CeFi platforms grew 24% in 2025. On the banking side: PayPal applied for a bank charter (industrial loan charter) in December 2025. The Fed replaced restrictions on state-chartered banks engaging in crypto activities. FDIC approved GENIUS Act stablecoin application procedures. The Blockchain Regulatory Certainty Act (bipartisan) is advancing toward US law. Grayscale’s 2026 Digital Asset Outlook explicitly calls this “the dawn of the institutional era.” The DeFi vs Traditional Banking comparison of 2030 will look fundamentally different from 2026 — and 2026 is the year the institutional foundation is being laid.

DeFi vs Traditional Banking: Decision Framework

The Core Question: What Does Your Financial Life Actually Need?

The DeFi vs Traditional Banking decision simplifies to three variables: your risk tolerance, the type of financial service you need, and your existing relationship with crypto. If you need FDIC-protected savings, unsecured credit, or everyday transaction banking — traditional banking is the answer. If you hold crypto assets and want to earn yield on them, transfer value internationally for pennies, or access financial services without identity documentation — DeFi is more suited to those specific jobs. For most people in 2026, the answer is not one or the other, but a thoughtfully designed mix of both.

Stick with Traditional Banking If:

- Your primary financial goals are capital preservation and safety — FDIC insurance and the regulated consumer protection framework exist specifically for you

- You need unsecured credit — mortgage, personal loan, car loan, or credit card — income-based credit underwriting is exclusively a traditional banking capability

- You are not comfortable managing private keys, understanding smart contracts, or absorbing the risk of irreversible transaction errors

- Your financial life is denominated entirely in fiat currency — payroll, rent, bills, taxes — all run through bank account rails that DeFi cannot replace in 2026

- You are in a jurisdiction where DeFi regulatory status is uncertain or where crypto-to-fiat conversion is difficult or restricted

- You are saving for retirement in a tax-advantaged account (401k, ISA, pension) — these regulated structures have no DeFi equivalent and provide significant tax benefits

Explore DeFi If:

- You already hold crypto assets and want to earn 5–15% APY on stablecoins rather than leaving them idle in a wallet or earning negligible bank interest

- You regularly send money internationally and are paying $25–50 per wire — DeFi stablecoin transfers offer 100x lower fees and 3.6-second settlement

- You are in a region where traditional banking is unavailable, expensive, or requires documentation you do not have — DeFi’s permissionless model serves you directly

- You want transparent, auditable financial infrastructure — 91% of DeFi apps display fees up front vs only 34% of banks; all protocol rules are publicly readable code

- You are a developer or fintech builder — DeFi’s composable protocol stack enables financial applications impossible to build on traditional banking infrastructure

- You understand the risks — smart contract exploits, liquidation mechanics, and private key management — and are comfortable accepting them for the yield and access advantages

DeFi vs Traditional Banking: Quick Decision Table

| Situation | Best Option | Key Reason |

|---|---|---|

| Saving $50K emergency fund | Traditional banking | FDIC insured, guaranteed accessible, no exploit risk |

| Earning yield on $10K USDC holdings | DeFi (Aave/Compound) | 5–15% APY vs 0.5–2% at banks; 2.5x advantage |

| Sending $500 to family in Philippines | DeFi stablecoins | $0.50 vs $25–50 fee; 3.6s vs 28 hours |

| Getting a mortgage | Traditional banking | Income-based credit; DeFi requires overcollateralisation |

| Trading ETH for USDC at 2am | DeFi (DEX) | 24/7, no account minimum, no broker approval |

| Banking without ID documentation | DeFi | Permissionless — wallet + internet only |

| Payroll and everyday spending | Traditional banking | Fiat rails; merchant acceptance; debit/credit cards |

| Corporate treasury cross-border payment | Hybrid (CeFi bridge + DeFi) | CEX compliance + stablecoin speed + regulatory clarity |

| Retirement savings | Traditional banking | Tax-advantaged wrappers, regulatory protection, stability |

| Maximum financial control and privacy | DeFi | Self-custody, no institution can freeze or restrict |

Frequently Asked Questions

DeFi and traditional banking have different risk profiles, not universally higher or lower risk. Traditional banking in the US saw $2.8 billion in fraud losses in H1 2025, but FDIC insurance and fraud recovery mechanisms mean most depositors did not bear those losses. DeFi saw $1.1 billion in exploits in the same period — but those losses were largely unrecoverable, with no insurance backstop and irreversible on-chain transactions. The key DeFi risk mitigation in 2026 is protocol auditing: audited protocols experience 94% fewer hacks, which is why checking audit status before depositing is non-negotiable.

Bug bounty programmes paid out $112 million in 2025. DeFi insurance platforms like Nexus Mutual covered $610 million in claims. The honest assessment: DeFi is meaningfully riskier than FDIC-insured bank deposits for capital you cannot afford to lose, but the risk is manageable and declining as the ecosystem matures. For yield-seeking investors comfortable with self-custody and smart contract risk, the 2.5x yield advantage compensates the risk for many use cases.

DeFi yields are higher for three interconnected reasons. First, DeFi lending protocols match lenders directly with borrowers algorithmically, eliminating the bank’s margin — the entire spread between deposit and lending rates flows to liquidity providers rather than being captured by an institution. Second, DeFi borrowing demand is driven by leveraged traders and yield farmers willing to pay high rates for short-term capital — these users create the demand that sustains the supply-side yields.

Third, DeFi protocols often supplement lending interest with governance token rewards as incentives for liquidity, further boosting headline yields. The 2.5x DeFi yield advantage vs traditional high-yield products has held through 2025 and into 2026, but DeFi yields are variable and can compress significantly when borrowing demand falls or when capital floods into protocols chasing high rates. The 0.9% effective real yield in US traditional savings accounts (after inflation adjustment) compared to DeFi’s 5–15% reflects both this market structure difference and the different risk profile that DeFi depositors accept in exchange for the yield premium.

Not in 2026, and probably not in the near term — but DeFi can already replace specific banking functions for specific users. DeFi cannot replace banks for: mortgage lending (requires income-based credit underwriting), tax-advantaged savings (401k, ISA, pension structures are regulatory products), everyday fiat spending (merchant acceptance, payroll, debit cards still run on bank rails), and dispute resolution (banks can reverse fraud; DeFi cannot). DeFi already outperforms banks for: cross-border remittances (100x cheaper, 28,000x faster), yield on crypto holdings, 24/7 trading access, and serving the globally unbanked.

The convergence underway in 2026 — 19% of DeFi platforms partnered with banks, 46% offering custodial wallets, the FDIC approving GENIUS Act stablecoin procedures — points toward a hybrid financial system rather than a replacement. The most probable outcome is that DeFi protocols become infrastructure layers that banks and fintech companies build products on top of, rather than standalone replacements for the banking system. Academic research from a January 2026 comparative analysis concluded: “DeFi and traditional banking systems are not necessarily adversaries but can evolve in parallel or even converge.”

TVL — Total Value Locked — is the primary metric for measuring the size and adoption of the DeFi ecosystem. It represents the total dollar value of crypto assets currently deposited into DeFi smart contracts across all protocols — lending pools, liquidity pools, staking contracts, and yield vaults. DeFi TVL sits at $130–140 billion in early 2026, down from its 2021 bull market peak but having significantly recovered from the post-FTX low of ~$50 billion.

In the DeFi vs Traditional Banking comparison, TVL is the closest equivalent to bank deposit volume — it represents the capital that users have committed to DeFi protocols rather than keeping in traditional bank accounts. The $130–140 billion in DeFi TVL vs $19.7 trillion in assets at the five largest US banks quantifies the current scale gap: DeFi is approximately 140 times smaller by this measure. However, the DeFi market is growing at 26.43% CAGR toward $770 billion by 2031, while traditional banking assets grow at low single-digit annual rates — the relative gap is narrowing structurally even if the absolute dollar difference remains enormous.

DeFi regulation is the fastest-moving legal development in financial services in 2026. In the US, the FDIC approved GENIUS Act stablecoin application procedures in December 2025, creating the first formal regulatory path for FDIC-supervised institutions to issue payment stablecoins. The Blockchain Regulatory Certainty Act (bipartisan, Senators Lummis and Wyden) is advancing — it clarifies that software developers and infrastructure providers who do not control user funds are not money transmitters, protecting developers from liability for protocols they build but do not operate. The Fed replaced its 2023 guidance restricting state-chartered banks from crypto activities, opening pathways for bank innovation.

In the EU, the MiCA (Markets in Crypto-Assets) framework is fully in force, providing the most comprehensive regulatory clarity for crypto assets globally — institutional capital is moving into MiCA-compliant on-chain channels. In practice for users: base-layer DeFi protocols (depositing to Aave, trading on Uniswap) remain largely unregulated in most jurisdictions, but the tax treatment of DeFi income is increasingly defined — in the US, DeFi yield is taxable income and DeFi trades are taxable events. The regulatory direction in 2026 is toward formalisation rather than prohibition — creating legal frameworks that allow DeFi innovation while applying anti-money-laundering and consumer protection standards.

A smart contract is a self-executing program stored on a blockchain — it automatically executes defined actions when predetermined conditions are met, with no human intermediary required. In the DeFi context, smart contracts replace each specific function that a bank performs. Aave’s lending smart contract: when you deposit USDC, it automatically calculates your interest rate based on the current supply-demand ratio in the pool and credits you with aUSDC tokens that accrue value in real time — no loan officer, no underwriter, no approval delay.

Uniswap’s AMM smart contract: when you want to trade ETH for USDC, it calculates the exchange rate from the liquidity pool reserves and executes the trade atomically in a single transaction — no market maker, no broker, no spread manipulation. MakerDAO’s CDP contract: when you deposit ETH as collateral, it mints DAI stablecoins up to your collateral-backed borrowing limit — automatically liquidating your collateral if the ETH price falls below the liquidation ratio. The critical difference from a bank: smart contracts execute exactly as coded, 24/7, without human discretion or error — but they also cannot be changed if they contain bugs, which is why the $1.1 billion in DeFi exploits in H1 2025 came 52% from smart contract vulnerabilities. Code is law — a feature and a risk simultaneously.

Stablecoins are cryptocurrencies designed to maintain a stable value, typically pegged 1:1 to the US dollar. USDC (Circle) and USDT (Tether) are fiat-backed — each token is backed by US dollar reserves held in regulated custodians, audited regularly. DAI (MakerDAO) is crypto-collateralised — maintained algorithmically through overcollateralised ETH deposits. Stablecoins form 62% of all collateral in DeFi lending platforms in 2025 and are the primary asset class for DeFi yield strategies — because they eliminate the price volatility risk of holding ETH or BTC while still accessing DeFi yields.

In the DeFi vs Traditional Banking comparison, stablecoins are the bridge: they allow users to hold dollar-denominated value in a self-custodial wallet (self-bank), earn DeFi yield on that value (outperform banks), and transfer it globally in seconds at negligible cost (outperform wire transfers) — all without giving custody to a bank. The FDIC’s December 2025 GENIUS Act stablecoin procedures and the Fed’s updated guidance on bank crypto activities signal that stablecoins are the specific DeFi instrument regulators are most focused on integrating into the traditional financial system, making 2026 the pivotal year for stablecoin regulatory clarity in the US.

The 5.4 billion globally unbanked or underbanked represent the single most compelling social argument for DeFi. They are excluded from traditional banking primarily by three barriers: documentation (78% of banks in emerging markets require in-person identity verification — many people lack government ID, proof of address, or utility bills), geographic access (91% of banking infrastructure investment is concentrated in G20 countries — rural populations in sub-Saharan Africa, Southeast Asia, and South Asia have no local bank branch), and minimum balance requirements (banks in many markets require minimum deposits that represent weeks of income for low-earning populations).

DeFi bypasses all three barriers: anyone with a smartphone and internet connection can create a wallet in minutes, access lending and savings protocols, and transact globally — no ID, no minimum deposit, no geographic restriction. The adoption data reflects this: 33% of DeFi users are in Asia (Vietnam, India, Philippines among top adopters), 21% in Latin America (Brazil, Argentina, Colombia), and 19% in Sub-Saharan Africa (Nigeria, Kenya). 53% of new wallet creations in 2025 came from mobile-first regions in Southeast Asia and Africa. DeFi’s financial inclusion potential is its most significant long-term social impact — and 2026 is the year that institutional infrastructure (regulated on-ramps, stablecoin frameworks, MiCA) is making that access safer and more durable.

The DeFi vs Traditional Banking comparison beyond 2026 points toward convergence rather than replacement. Several structural trends define the trajectory. Regulatory integration: as US and EU frameworks solidify around stablecoins, DeFi protocols, and tokenised assets, institutional capital can move on-chain under clear legal frameworks — Grayscale projects “bipartisan crypto market structure legislation to become US law in 2026,” bringing institutional banking and DeFi infrastructure into the same regulated perimeter.

Real-world asset tokenisation: the tokenisation of bonds, real estate, equities, and trade finance on-chain is advancing — Centrifuge, BlackRock (tokenised Treasury fund), and others are building the DeFi-traditional finance bridge through tokenised instruments that operate under both on-chain settlement and regulated legal frameworks. Banking adoption of blockchain settlement: as FedNow (US real-time payments), SEPA Instant (EU), and cross-border blockchain settlement mature, the speed advantage of DeFi over traditional banking will narrow. The DeFi TVL growth from $130–140 billion toward $770 billion by 2031 at 26.43% CAGR represents capital flowing from traditional financial instruments into DeFi protocols — not a revolution, but a structural reallocation. The most likely 2030 scenario: a financial system where DeFi protocols handle settlement and yield infrastructure while regulated institutions provide the compliance, insurance, credit, and consumer protection layers on top — a hybrid that captures the efficiency of code-based finance and the safety of regulatory oversight.

DeFi vs Traditional Banking: Final Takeaways for 2026

The DeFi vs Traditional Banking comparison in 2026 reaches a clear conclusion: these are not competing systems for the same users — they are complementary systems optimised for different financial jobs. Traditional banking excels at protected capital, credit access, and fiat integration. DeFi excels at yield generation, global access, and transparent programmable finance.

Traditional Banking — Key Takeaways:

- $19.7 trillion in assets at the 5 largest US banks

- FDIC insured up to $250K per depositor — unmatched safety net

- Income-based unsecured credit — mortgages, personal loans

- 0.5–2% APY standard savings; ~4.5% high-yield online banks

- 28-hour international wire; $25–50 per transfer

- 2026: integrating stablecoins, tokenised assets, DeFi protocols

DeFi — Key Takeaways:

- $238.54B market in 2026 → $770.56B by 2031 (26.43% CAGR)

- TVL $130–140B; 20M+ users; DEX volume $462B/month

- 5–15% APY stablecoin yield — 2.5x traditional high-yield

- 3.6 second settlement; cents in fees; 24/7 permissionless access

- No FDIC insurance; $1.1B exploits H1 2025; irreversible errors

- 2026: GENIUS Act, MiCA, institutional era — regulatory clarity arriving

Practical Recommendation for 2026:

Keep your emergency fund and primary savings in FDIC-insured bank accounts — the safety guarantee is worth more than any yield differential for capital you cannot afford to lose. Explore DeFi for crypto assets you already hold: earning 5–15% APY on stablecoins via Aave or Compound is the most accessible, highest-impact DeFi use case for most users. If you send money internationally regularly, DeFi stablecoin transfers at cents vs $25–50 per wire is an immediate, practical saving with no ideological commitment required. As the GENIUS Act stablecoin framework and US crypto market structure legislation take shape through 2026, the DeFi vs Traditional Banking comparison becomes progressively less adversarial and more about choosing the right tool for each financial job in an increasingly hybrid system.

Related Topics Worth Exploring

CBDC vs Cryptocurrency

Central Bank Digital Currencies are the traditional banking system’s direct response to DeFi and crypto — government-issued digital money on centralised ledgers. Understanding the differences between a CBDC, a stablecoin, and a decentralised cryptocurrency is essential context for the future of the DeFi vs Traditional Banking comparison.

Open Banking vs Traditional Banking APIs

Open Banking is traditional banking’s regulatory mandate to open its data and infrastructure to third parties via APIs — a different but complementary path to financial innovation alongside DeFi. The EU’s FIDA Open Finance regulation advancing in 2026 makes this the other major structural change in banking worth understanding alongside DeFi.

Stablecoins vs Traditional Payments

Stablecoins are the bridge between DeFi and traditional banking — the instrument most likely to achieve mainstream adoption as a payment rail in 2026. Understanding how USDC, DAI, and PayPal USD compare to Visa, SWIFT, and bank transfers positions the DeFi vs Traditional Banking debate in its most practical current-year context.